The overpayment scam is a specific type of online selling scam where a buyer sends you a check for significantly more than your asking price, then asks you to wire back the difference. The check is fraudulent. By the time your bank discovers it, the money you sent is gone. This scam targets sellers on Facebook Marketplace, Craigslist, rental platforms, and freelance job sites—and it works because of a timing gap between when a bank makes funds available and when it actually verifies a check.

What Is the Overpayment Scam?

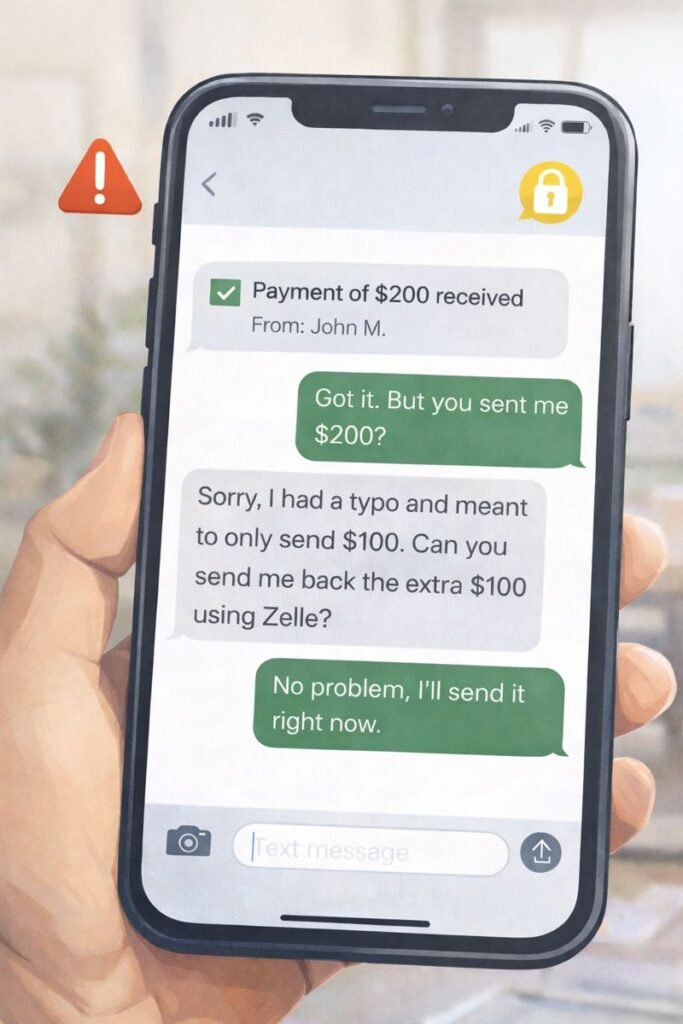

The overpayment scam targets people selling items or services online. A buyer contacts you, agrees to your price without negotiation, and then sends a check—usually a cashier’s check or money order—for significantly more than you asked. They explain the overpayment with a plausible reason: they accidentally wrote the wrong amount, their employer issued the check with travel expenses included, or the extra money covers shipping through a third party.

The buyer then asks you to deposit the check and send back the difference via wire transfer, Zelle, or Venmo. Here’s what makes this fake check overpayment scheme so effective: the check looks completely real. It may even clear your bank’s initial processing and appear as available funds within 24 hours. But the check is fraudulent, and when your bank eventually verifies it with the issuing bank—a process that takes 7 to 10 business days—the deposit is reversed. The money you already sent back is long gone.

This scam appears wherever people sell things: Facebook Marketplace, Craigslist, eBay, Nextdoor, rental listings, and freelance job postings. The setup changes depending on context, but the core mechanism never changes—you receive more than expected, you send some back, and the original payment fails.

How the Overpayment Scam Usually Works

The scam starts with a buyer expressing strong interest in what you’re selling. They don’t negotiate price, agree quickly, and communicate mostly by text or email rather than calling or meeting in person. They may claim to be out of town, deployed overseas, traveling for work, or unable to meet locally—which explains why they need to pay by check instead of cash or a local payment method.

A check arrives in the mail with a noticeably higher amount than your asking price. The buyer follows up with an apology and an explanation: their bookkeeper made an error, the check was pre-printed with a larger amount, or the extra is for you to pay a shipper, moving company, or contractor on their behalf. They ask you to deposit it and send the excess—usually by wire transfer, Zelle, Venmo, or gift cards—immediately.

The urgency is deliberate. Scammers know that waiting increases the chance you’ll call your bank or think things through. They often follow up repeatedly asking whether you’ve sent the money, sometimes adding pressure by claiming they need the funds urgently for another purpose. If you hesitate, they may sweeten the deal by offering extra payment or even claiming to pay first-month rent on a property or a large project deposit.

When you deposit the check, your bank makes the funds available within 1-2 business days. This availability is not verification. Federal law (Regulation CC) requires banks to make checks available quickly, but this doesn’t mean they’ve verified the check with the issuing bank. That verification process happens in the background and takes 7 to 10 business days. By the time the check is confirmed as fraudulent and reversed, your wire transfer or Zelle payment is already in the scammer’s account.

The key insight: available funds and cleared funds are not the same thing. You’ll see the money in your account, but it’s still provisional. Once you send money out, you can’t get it back when the check bounces.

Why Overpayment Scams Still Work

The overpayment check scam succeeds because it exploits a gap between banking speed and banking verification. Your bank’s system is built to move money fast—that’s convenient for legitimate transactions. But scammers use that speed against you. You see funds available, you trust the appearance, and you send money before the actual verification completes.

Psychology plays a major role too. Most people trust cashier’s checks because they believe a bank has already verified the funds. In reality, a cashier’s check is just a promise from the issuing bank, and scammers can forge it convincingly. When a buyer overpays with a polite excuse, most sellers believe the explanation rather than question the entire transaction—it feels like an honest mistake, not fraud.

Urgency works because it short-circuits thinking. When a buyer repeatedly asks “Have you sent the money yet?” or claims they need it for an urgent move or expense, you feel pressure to act. You think about the deal falling through, about looking unreliable to the buyer, or about disappointing them. That emotional pressure overrides caution. Scammers exploit this deliberately.

Finally, the scam works because the person on the other end seems real. They communicate, ask questions, sometimes negotiate minor details. They’re not obviously a criminal. This appearance of legitimacy makes the scenario feel plausible—which is exactly what makes it dangerous.

Where Overpayment Scams Target Online Sellers

Facebook Marketplace and Craigslist. These platforms attract the most overpayment scams. Sellers listing furniture, electronics, vehicles, collectibles, and other high-value items are frequently approached by “buyers” who prefer to pay by check and can’t meet in person. The open nature of these platforms makes it easy for scammers to contact many sellers quickly.

Rental listings. Landlords and property managers listing rooms, apartments, vacation rentals, or commercial space receive inquiries from “tenants” or “business users” who send a deposit check for more than the first month’s rent. They ask the landlord to forward the overage to a moving company, previous landlord, or property manager. This variant often includes the scammer claiming they’re relocating urgently for a job.

Freelance and remote work platforms. Someone hires you for a design, writing, administrative, or coding project and sends an advance payment check larger than your quoted rate. They ask you to pay a subcontractor, purchase software, or cover set-up costs from the difference. This version often overlaps with fake job offer scams.

Ticket and event sales. People selling concert tickets, sports tickets, festival passes, or other event admission through personal listings receive overpayment checks from buyers who claim the extra amount covers shipping, a ticket broker fee, or resale platform fees.

Vehicle sales. Private car sellers are frequent targets. A buyer expresses interest in a vehicle, offers to send a cashier’s check unseen, and the check arrives for more than the asking price with a story about needing you to pay a shipping company or inspection service.

How to Protect Yourself From Overpayment Scams

Insist on safe payment methods. Only accept payment methods that don’t involve reversal risk. For in-person transactions, cash is safest. For online sales, use payment platforms with buyer-seller protection like PayPal Goods & Services, Venmo (explicitly for goods/services), Square Cash, or payment systems built into the marketplace itself. These platforms verify both parties and allow disputes to be resolved without check reversals.

Never accept checks from buyers you haven’t met. Cashier’s checks and money orders can be forged just like any other document. If a buyer insists on paying by check, insist on meeting in person at a neutral location—ideally a police station parking lot, which many departments offer as a safe exchange point. Verify the check’s legitimacy on the spot using the bank’s app or website before you hand over the item. For vehicles and high-value items, this step is non-negotiable.

Wait for full clearance before sending anything. If you receive a check for any reason, do not ship an item, deliver a service, or send any money back until the check has fully cleared. Full clearing takes 7 to 10 business days. Call your bank and ask explicitly: “Has this check been verified as legitimate by the issuing bank and become part of my settled balance?” Available funds in your account is not the same as a cleared check. Most banks will confirm this in writing if you ask.

Never send money back before verification. A legitimate buyer who accidentally overpays can request a refund after the check clears. No honest buyer will pressure you to wire back money immediately after a check deposit. If someone is pushing you to act fast, that pressure itself is a warning sign. Review What Real Companies Will Never Ask You To Do for more context on recognizing pressure tactics.

Be skeptical of buyers who avoid in-person meetings. Legitimate buyers often prefer to see an item, meet the seller, and exchange cash. Scammers deliberately avoid this because they can’t offer a real check in person—it would be verified immediately. If a buyer consistently avoids meeting, communicates only by text, offers more than your asking price, and wants to pay by check, that combination is a major red flag.

Use marketplace protections. Platforms like Facebook Marketplace, eBay, and others offer seller protection policies. Sell through the marketplace’s built-in payment system when possible rather than arranging payment outside the platform. These systems typically don’t allow check payments, which eliminates the risk entirely.

What to Do If You’ve Already Sent Money

Contact your bank immediately. Explain that you deposited a check you now believe is fraudulent and that you sent money out before it cleared. Ask whether the wire transfer, Zelle payment, or other transfer can be recalled or reversed. Speed matters—the sooner you call, the slightly better your odds of recovery. Wire transfers are rarely reversible once processed, but some payments made through apps can be frozen before being cashed out.

Contact payment platforms directly. If you sent money via Zelle, Venmo, or Cash App, report the fraud to the platform immediately. While these apps typically don’t reverse completed transfers, reporting creates an official record and may help freeze the scammer’s account or prevent them from moving the money. Include transaction details, timestamps, and the recipient’s account information.

If you sent gift cards. Call the gift card issuer with the card numbers and codes as soon as possible. Explain the fraud situation. Some issuers can freeze the remaining balance if you act quickly enough, before the scammer has spent the full amount. This is one situation where speed can make a real difference.

Report the scam to the FTC. Go to ReportFraud.ftc.gov and file a complaint. Include all details about the transaction, the buyer’s contact information, the check details if you have them, and the payment method you used to send money back. The FTC uses these reports to identify patterns and warn the public.

Report to the marketplace. Contact the platform where you met the buyer (Facebook, Craigslist, eBay, etc.) and report the buyer’s account and the scam. Provide the conversation history and transaction details. This helps get the scammer’s account removed and protects other sellers from the same person or group.

File a postal inspection report if applicable. If the check was mailed to you, it constitutes mail fraud. File a report with the US Postal Inspection Service at postalinspectors.uspis.gov. Include the envelope, any identifying information about the check, and your account of the scam.

For a deeper understanding of why checks appear to clear before bouncing, see our Fake Check Scam article. For broader next steps after being scammed, see I Got Scammed — Now What?

Key Takeaway

The overpayment scam works because it creates false legitimacy. A real check from a real bank sounds safe. Quick availability feels like verification. And an apologetic buyer with a reasonable story feels trustworthy. But this combination—buyer sends too much money, asks you to wire back the difference, and pressures you to act fast—is a deliberate fraud pattern, not an honest mistake. Protect yourself by insisting on safe payment methods, meeting in person when possible, waiting for full check clearance, and never sending money back before verification. If the scenario feels off, trust that instinct.